Global Medical Electronics Market: By Component, By Medical Procedure, Medical Device Classification, By End User Products, By Application, By Region & Segmental Insights Trends and Forecast, 2024 – 2034

- Industry: Healthcare

- Report ID: TNR-110-1115

- Number of Pages: 420

- Table/Charts : Yes

- June, 2024

- Base Year : 2024

- No. of Companies : 10+

- No. of Countries : 29

- Views : 10160

- Covid Impact Covered: Yes

- War Impact Covered: Yes

- Formats : PDF, Excel, PPT

Medical electronics refers to the application of electronic devices and systems in healthcare to diagnose, monitor, and treat medical conditions. This field encompasses a wide range of technologies, including imaging systems (like MRI and CT scanners), diagnostic equipment (such as ECG and blood glucose monitors), therapeutic devices (like pacemakers and defibrillators), and advanced wearable health tech. These devices enhance the accuracy and efficiency of medical diagnostics and treatments, improving patient outcomes and streamlining healthcare processes.

Advancements in medical electronics are driven by innovations in microelectronics, sensor technology, and wireless communication, enabling the development of more compact, efficient, and powerful medical devices. For instance, portable ultrasound devices and telemedicine platforms have revolutionized remote patient care, making healthcare more accessible. Additionally, the integration of AI and machine learning in medical electronics is transforming data analysis and predictive diagnostics, leading to more personalized and effective treatment plans. Overall, medical electronics plays a crucial role in modern healthcare, continuously evolving to meet the growing demands of patient care and medical research.

The demand for medical electronics is driven by several key factors. Firstly, the aging global population increases the need for advanced diagnostic and monitoring devices to manage chronic conditions. Technological advancements, such as the miniaturization of electronic components and the integration of artificial intelligence, enhance device capabilities and patient outcomes.

The rise of telemedicine and remote patient monitoring, accelerated by the COVID-19 pandemic, further fuels demand for portable and wearable medical electronics. Additionally, increasing healthcare spending and the emphasis on early diagnosis and preventive care promote the adoption of sophisticated medical electronics. These factors collectively drive the growth of the medical electronics market, making it a critical component of modern healthcare infrastructure.

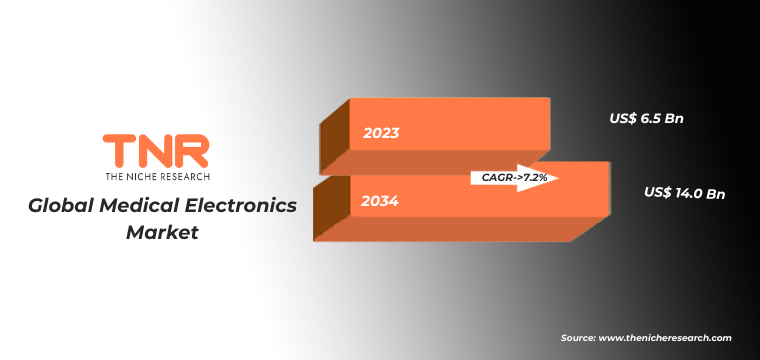

In Terms of Revenue, the Global Medical Electronics Market was Worth US$ 6.5 Bn in 2023, Anticipated to Witness CAGR of 7.2% During 2024 – 2034.

Global Medical Electronics Market Dynamics

Aging Population: The global increase in the elderly population heightens the need for advanced medical electronics to manage age-related diseases, chronic conditions, and enhance quality of life through improved diagnostics and monitoring.

Technological Advancements: Innovations such as AI, machine learning, and the miniaturization of components enhance the functionality, efficiency, and portability of medical devices, driving their adoption in various healthcare settings. The rise of telemedicine, spurred by the COVID-19 pandemic, has increased the demand for portable and wearable medical electronics, enabling remote patient care and continuous health monitoring.

Personalized Medicine: Advancements in medical electronics, particularly in diagnostics and data analytics, enable personalized treatment plans tailored to individual patient profiles, improving treatment efficacy and patient outcomes. Developing regions with growing healthcare infrastructure and increased access to medical technology represent significant growth opportunities for the medical electronics market.

High Costs: The high development and manufacturing costs of advanced medical electronics can limit their accessibility and adoption, particularly in cost-sensitive markets and developing regions. Stringent regulatory requirements and the need for compliance with diverse international standards can pose challenges for the development and commercialization of medical electronics.

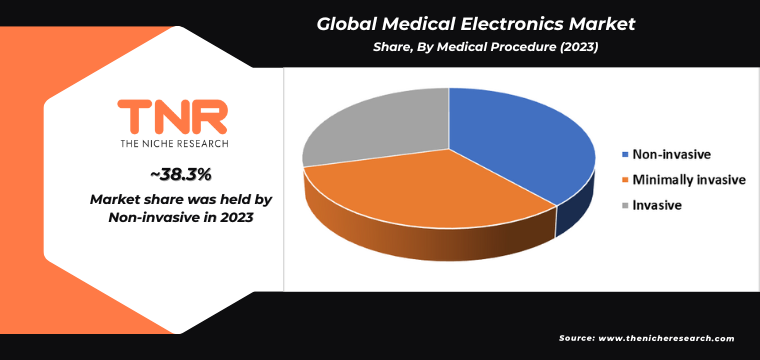

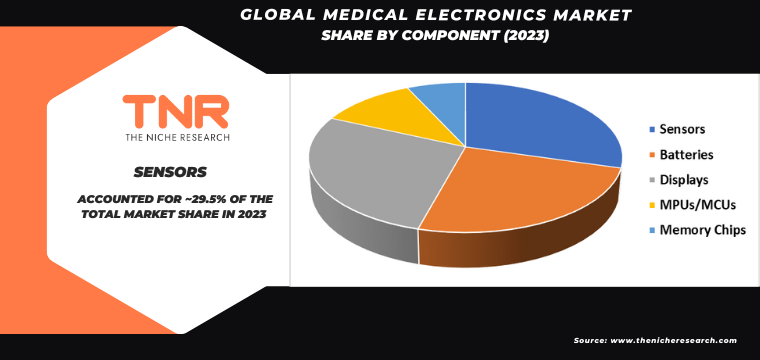

Sensor Segment Has Garnered Major Market Share in the Global Medical Electronics Market During the Forecast Period (2024 – 2034).

Sensors are pivotal in the medical electronics market, driving significant advancements and growth. The increasing prevalence of chronic diseases, such as diabetes and cardiovascular conditions, necessitates continuous and accurate monitoring, boosting the demand for sensor-integrated medical devices. For instance, glucose monitoring sensors are essential for diabetes management, providing real-time data and enhancing patient care. Technological advancements in sensor technology, including miniaturization and improved sensitivity, enable the development of more efficient and less invasive medical devices.

These innovations support the growing trend of wearable health tech, which relies heavily on sensors to track vital signs and other health metrics continuously. The rise of telemedicine and remote patient monitoring further accelerates the demand for advanced sensors, facilitating high-quality care outside traditional healthcare settings. Additionally, aging populations in many regions require more frequent health monitoring, driving the need for sensor-based medical electronics. Overall, the integration of advanced sensors in medical devices enhances diagnostic accuracy, patient monitoring, and overall healthcare outcomes, fueling their demand in the medical electronics market.

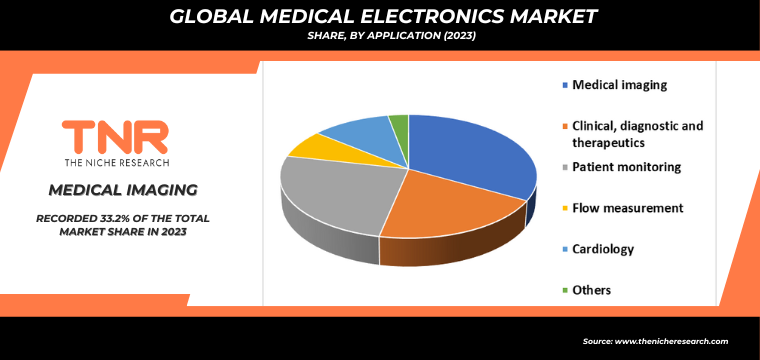

By Application Medical Imagining Segment had the Highest Share in the Global Medical Electronics Market in 2023.

The increasing prevalence of chronic diseases, such as cancer and cardiovascular conditions, necessitates advanced diagnostic tools for early detection and treatment planning. Innovations in imaging technologies, including MRI, CT, and ultrasound, enhance the accuracy and efficiency of diagnostics, contributing to their growing adoption. Furthermore, the aging global population requires frequent medical assessments, boosting the demand for reliable and advanced imaging solutions.

Technological advancements in medical electronics, such as digital imaging and artificial intelligence, improve image quality and enable more precise analysis, driving further demand. The shift towards minimally invasive procedures also relies heavily on accurate imaging, increasing the use of advanced medical imaging devices. Additionally, the rise of telemedicine and remote diagnostics has accelerated the need for portable imaging solutions, enabling healthcare providers to deliver high-quality care in diverse settings. These factors collectively drive the robust growth of the medical imaging segment within the medical electronics market.

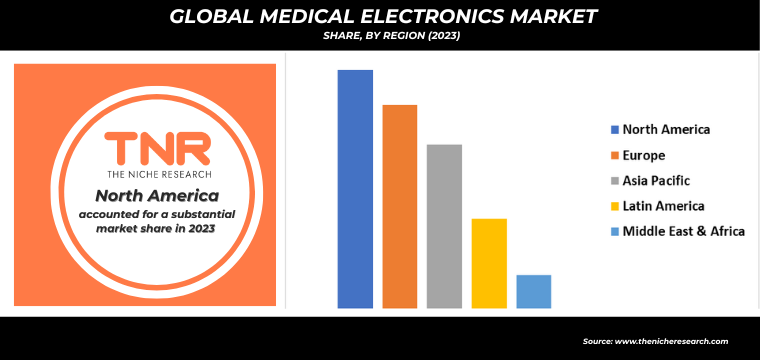

By Region, North America dominated the Global Medical Electronics Market in 2023.

In North America, the medical electronics market is driven by several key factors. Firstly, the region’s aging population increases the demand for advanced medical devices to manage chronic diseases and age-related conditions. Technological innovations, particularly in areas like wearable health tech, telemedicine, and AI-driven diagnostics, enhance patient care and drive market growth. The region’s robust healthcare infrastructure supports the rapid adoption and integration of cutting-edge medical electronics. Additionally, high healthcare spending in North America ensures substantial investments in new medical technologies.

Government initiatives and policies promoting digital health and the use of advanced medical electronics further stimulate market demand. The rise of telehealth, accelerated by the COVID-19 pandemic, has significantly boosted the need for portable and remote monitoring devices. Moreover, the increasing prevalence of chronic diseases, such as diabetes and cardiovascular conditions, necessitates continuous monitoring and advanced diagnostic tools, driving the demand for medical electronics in North America.

Competitive Landscape: Global Medical Electronics Market:

- Canon Medical Systems

- Drägerwerk AG & Co. KGaA

- Esaote SpA

- Fujifilm Corporation

- GE Healthcare

- Getinge Inc.

- Hologic Inc.

- Koninklijke Philips NV

- McKesson Corporation

- Medtronic PLC

- Olympus Corporation

- Siemens Healthcare GmbH

- Other Industry Participants

Global Medical Electronics Market Scope

| Report Specifications | Details |

| Market Revenue in 2023 | US$ 6.5 Bn |

| Market Size Forecast by 2034 | US$ 14.0 Bn |

| Growth Rate (CAGR) | 7.2% |

| Historic Data | 2016 – 2022 |

| Base Year for Estimation | 2023 |

| Forecast Period | 2024 – 2034 |

| Report Inclusions | Market Size & Estimates, Market Dynamics, Competitive Scenario, Trends, Growth Factors, Market Determinants, Key Investment Segmentation, Product/Service/Solutions Benchmarking |

| Segments Covered | By Component, By Medical Procedure, Medical Device Classification, By End User Products, By Application, By Region |

| Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | U.S., Canada, Mexico, Rest of North America, France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe, China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific, Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa, Brazil, Argentina, Rest of Latin America |

| Key Players | Canon Medical Systems, Drägerwerk AG & Co. KGaA, Esaote SpA, Fujifilm Corporation, GE Healthcare, Getinge Inc., Hologic Inc., Koninklijke Philips NV, McKesson Corporation, Medtronic PLC, Olympus Corporation, Siemens Healthcare GmbH |

| Customization Scope | Customization allows for the inclusion/modification of content pertaining to geographical regions, countries, and specific market segments. |

| Pricing & Procurement Options | Explore purchase options tailored to your specific research requirements |

| Contact Details | Consult With Our Expert

Japan (Toll-Free): +81 663-386-8111 South Korea (Toll-Free): +82-808- 703-126 Saudi Arabia (Toll-Free): +966 800-850-1643 United Kingdom: +44 753-710-5080 United States: +1 302-232-5106 E-mail: askanexpert@thenicheresearch.com

|

Global Medical Electronics Market

By Component

- Sensors

- Batteries

- Displays

- MPUs/MCUs

- Memory Chips

By Medical Procedure

- Non-invasive

- Minimally invasive

- Invasive

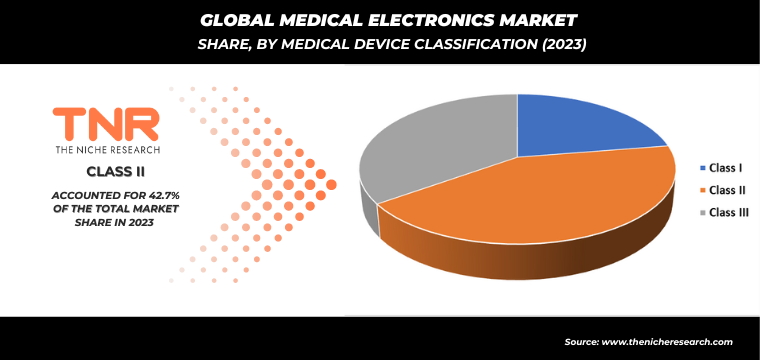

By Medical Device Classification

- Class I

- Class II

- Class III

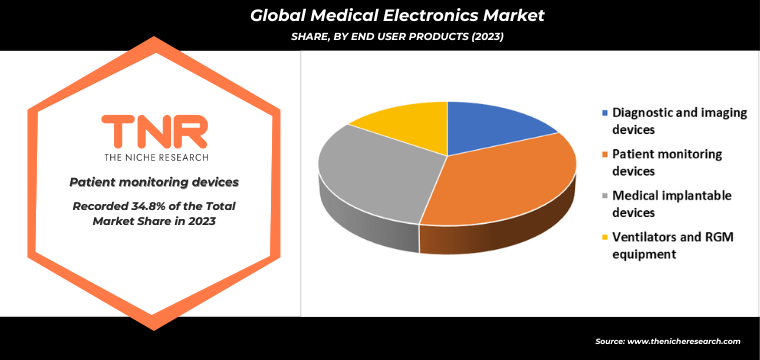

By End User Products

- Diagnostic and imaging devices

- Patient monitoring devices

- Medical implantable devices

- Ventilators and RGM equipment

By Application

- Medical imaging

- Clinical, diagnostic and therapeutics

- Patient monitoring

- Flow measurement

- Cardiology

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

Report Layout:

Table of Contents

Note: This ToC is tentative and can be changed according to the research study conducted during the course of report completion.

**Exclusive for Multi-User and Enterprise User.

Global Medical Electronics Market

By Component

- Sensors

- Batteries

- Displays

- MPUs/MCUs

- Memory Chips

By Medical Procedure

- Non-invasive

- Minimally invasive

- Invasive

By Medical Device Classification

- Class I

- Class II

- Class III

By End User Products

- Diagnostic and imaging devices

- Patient monitoring devices

- Medical implantable devices

- Ventilators and RGM equipment

By Application

- Medical imaging

- Clinical, diagnostic and therapeutics

- Patient monitoring

- Flow measurement

- Cardiology

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

The Niche Research approach encompasses both primary and secondary research methods to provide comprehensive insights. While primary research is the cornerstone of our studies, we also incorporate secondary research sources such as company annual reports, premium industry databases, press releases, industry journals, and white papers.

Within our primary research, we actively engage with various industry stakeholders, conducting paid interviews and surveys. Our meticulous analysis extends to every market participant in major countries, allowing us to thoroughly examine their portfolios, calculate market shares, and segment revenues.

Our data collection primarily focuses on individual countries within our research scope, enabling us to estimate regional market sizes. Typically, we employ a bottom-up approach, meticulously tracking trends in different countries. We analyze growth drivers, constraints, technological innovations, and opportunities for each country, ultimately arriving at regional figures.Our process begins by examining the growth prospects of each country. Building upon these insights, we project growth and trends for the entire region. Finally, we utilize our proprietary model to refine estimations and forecasts.

Our data validation standards are integral to ensuring the reliability and accuracy of our research findings. Here’s a breakdown of our data validation processes and the stakeholders we engage with during our primary research:

- Supply Side Analysis: We initiate a supply side analysis by directly contacting market participants, through telephonic interviews and questionnaires containing both open-ended and close-ended questions. We gather information on their portfolios, segment revenues, developments, and growth strategies.

- Demand Side Analysis: To gain insights into adoption trends and consumer preferences, we reach out to target customers and users (non-vendors). This information forms a vital part of the qualitative analysis section of our reports, covering market dynamics, adoption trends, consumer behavior, spending patterns, and other related aspects.

- Consultant Insights: We tap into the expertise of our partner consultants from around the world to obtain their unique viewpoints and perspectives. Their insights contribute to a well-rounded understanding of the markets under investigation.

- In-House Validation: To ensure data accuracy and reliability, we conduct cross-validation of data points and information through our in-house team of consultants and utilize advanced data modeling tools for thorough verification.

The forecasts we provide are based on a comprehensive assessment of various factors, including:

- Market Trends and Past Performance (Last Five Years): We accurately analyze market trends and performance data from preceding five years to identify historical patterns and understand the market’s evolution.

- Historical Performance and Growth of Market Participants: We assess the historical performance and growth trajectories of key market participants. This analysis provides insights into the competitive landscape and individual company strategies.

- Market Determinants Impact Analysis (Next Eight Years): We conduct a rigorous analysis of the factors that are projected to influence the market over the next eight years. This includes assessing both internal and external determinants that can shape market dynamics.

- Drivers and Challenges for the Forecast Period:Identify the factors expected to drive market growth during the forecast period, as well as the challenges that the industry may face. This analysis aids in deriving an accurate growth rate projection.

- New Acquisitions, Collaborations, or Partnerships: We keep a close watch on any new acquisitions, collaborations, or partnerships within the industry. These developments can have a significant impact on market dynamics and competitiveness.

- Macro and Micro Factors Analysis:A thorough examination of both macro-level factors (e.g., economic trends, regulatory changes) and micro-level factors (e.g., technological advancements, consumer preferences) that may influence the market during the forecast period.

- End-User Sentiment Analysis: To understand the market from the end-user perspective, we conduct sentiment analysis. This involves assessing the sentiment, preferences, and feedback of the end-users, which can provide valuable insights into market trends.

- Perspective of Primary Participants: Insights gathered directly from primary research participants play a crucial role in shaping our forecasts. Their perspectives and experiences provide valuable qualitative data.

- Year-on-Year Growth Trend: We utilize a year-on-year growth trend based on historical market growth and expected future trends. This helps in formulating our growth projections, aligning them with the market’s historical performance.

Research process adopted by TNR involves multiple stages, including data collection, validation, quality checks, and presentation. It’s crucial that the data and information we provide add value to your existing market understanding and expertise. We have also established partnerships with business consulting, research, and survey organizations across regions and globally to collaborate on regional analysis and data validation, ensuring the highest level of accuracy and reliability in our reports.