Global Opto-Semiconductors Market By Type, By End Use Industry, By Region & Segmental Insights Trends and Forecast, 2024 – 2034

- Industry: Semiconductors & Electronics

- Report ID: TNR-110-1290

- Number of Pages: 420

- Table/Charts : Yes

- September, 2024

- Base Year : 2024

- No. of Companies : 10+

- No. of Countries : 29

- Views : 10054

- Covid Impact Covered: Yes

- War Impact Covered: Yes

- Formats : PDF, Excel, PPT

Opto-semiconductors are specialized semiconductor devices that convert electrical signals into optical signals and vice versa, playing a vital role in technologies like LEDs, laser diodes, photodiodes, and optical sensors. These components are fundamental to various applications, including lighting, displays, optical communication, and sensing systems. The evolution of opto-semiconductors began in the 1960s with the development of early LEDs, primarily used as indicators due to their limited light output. Advances in materials like gallium arsenide (GaAs) and gallium phosphide (GaP) expanded their capabilities, leading to broader applications in the following decades.

By the 1990s, LEDs found their way into consumer electronics, and laser diodes became crucial for optical communication and data transmission. The 2010s saw the rise of high-efficiency LEDs and the integration of opto-semiconductors into smart devices, enhancing features like ambient light detection and facial recognition. In recent years, innovations such as quantum dots and micro-LEDs have further pushed the boundaries of opto-semiconductors, making them indispensable in emerging technologies like autonomous vehicles, 5G networks, and healthcare devices. This continuous advancement in material science and technology has transformed opto-semiconductors from simple components into critical enablers of modern technological progress across various industries.

Global Opto-Semiconductors Market Size and Growth Projections

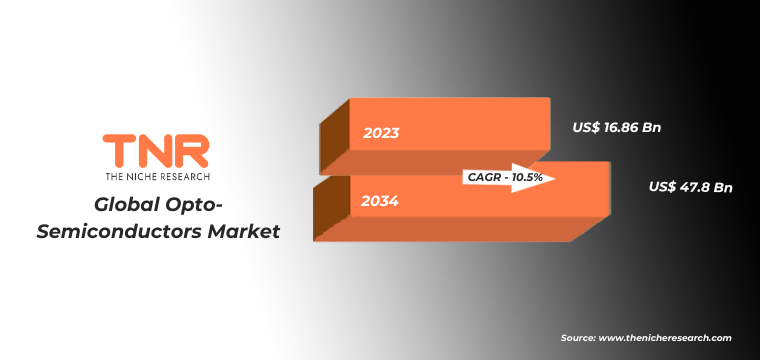

As of 2023, the global opto-semiconductors market is valued at approximately USD 16.86 billion and is projected to grow at a CAGR of 10.5% from 2024 to 2034. By 2034, the global opto-semiconductors market is expected to reach a value of USD 47.8 billion. This robust growth is driven by the increasing demand for opto-semiconductors in various applications, particularly in the automotive, consumer electronics, and industrial sectors.

Global Opto-Semiconductors Market Key Market Segments

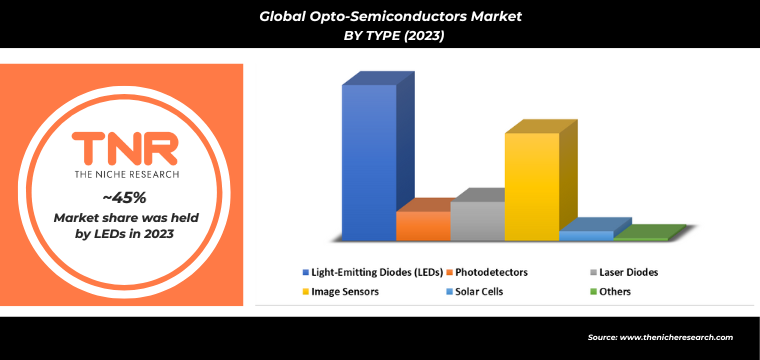

LEDs represent the largest segment within the opto-semiconductors market, holding a substantial market share of 45% in 2023. This dominance is largely driven by the widespread adoption of LED technology across various sectors, including lighting, displays, and automotive applications. LEDs have become the preferred choice for lighting solutions due to their energy efficiency, longer lifespan, and environmental benefits. For instance, the global shift towards energy-efficient lighting, driven by government regulations and consumer awareness, has significantly bolstered the demand for LEDs. Countries like China, which is the largest producer and consumer of LEDs, have played a pivotal role in this growth. China’s LED industry benefits from government incentives, robust manufacturing capabilities, and a strong export market.

In the automotive sector, the increasing integration of LED lighting in vehicles for headlights, taillights, and interior illumination has further fueled market growth. Companies like Osram Opto Semiconductors GmbH and Samsung Electronics Co., Ltd. are leading players in this segment, offering advanced LED solutions for automotive and consumer electronics applications. Osram, for instance, has been at the forefront of developing high-performance automotive LEDs, which are increasingly used in premium vehicles due to their superior brightness and energy efficiency.

In the automotive sector, the increasing integration of LED lighting in vehicles for headlights, taillights, and interior illumination has further fueled market growth. Companies like Osram Opto Semiconductors GmbH and Samsung Electronics Co., Ltd. are leading players in this segment, offering advanced LED solutions for automotive and consumer electronics applications. Osram, for instance, has been at the forefront of developing high-performance automotive LEDs, which are increasingly used in premium vehicles due to their superior brightness and energy efficiency.

Moreover, the growing trend towards smart lighting systems, particularly in regions like North America and Europe, has contributed to the rising demand for LEDs. In these regions, government bodies have implemented stringent energy efficiency regulations, such as the European Union’s ban on halogen bulbs, which has driven the replacement of traditional lighting systems with LEDs. The increasing focus on sustainability and the reduction of carbon footprints have made LEDs the lighting solution of choice, further bolstering their market presence.

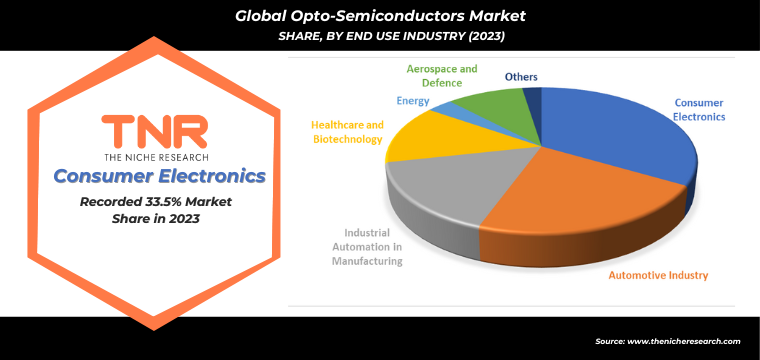

In 2023, consumer electronics accounted for the largest market share within the global opto-semiconductors market, representing approximately 33% of the total market. This significant share is driven by the extensive use of opto-semiconductor components, such as LEDs, laser diodes, and optical sensors, in a wide range of consumer electronics devices. These devices include smartphones, tablets, televisions, gaming consoles, and wearable technology, all of which rely on opto-semiconductors for functions like display illumination, camera modules, facial recognition, and ambient light sensing.

Smartphones, in particular, have been a major contributor to this market share. The integration of advanced optical sensors for features like facial recognition and augmented reality (AR) has spurred demand. Companies like Apple Inc. and Samsung Electronics Co., Ltd. have been at the forefront of incorporating cutting-edge opto-semiconductors into their flagship devices. For example, Apple’s Face ID technology, which uses a sophisticated TrueDepth camera system, relies heavily on opto-semiconductors for 3D facial recognition. This technology not only enhances security but also enables innovative applications in AR.

In addition, the demand for high-quality displays in televisions and monitors has led to the increased use of LEDs and organic LEDs (OLEDs) in consumer electronics. OLED technology, which offers superior contrast ratios and deeper blacks compared to traditional LED displays, has been widely adopted by companies like LG Electronics and Sony Corporation in their premium television models. These advancements have driven the market share of consumer electronics within the opto-semiconductors industry.

The rising popularity of wearable technology, such as fitness trackers and smartwatches, has further fuelled the growth of opto-semiconductors in this segment. These devices often incorporate optical sensors to monitor heart rates, blood oxygen levels, and other health metrics. The increasing consumer interest in health and wellness, coupled with the trend towards connected devices, has strengthened the demand for opto-semiconductors in wearable tech.

Furthermore, ongoing evolution of smart home devices, including smart speakers, lighting systems, and security cameras, continues to drive demand for opto-semiconductors. Companies like Google and Amazon have integrated optical sensors and LEDs into their smart home ecosystems, enhancing user experience through improved interaction and energy efficiency.

The consumer electronics segment’s market share, at 33% in 2023, underscores the critical role opto-semiconductors play in modern electronics. As the industry continues to innovate and develop more advanced and integrated technologies, the demand for these components is expected to grow, further solidifying the consumer electronics sector’s dominance within the opto-semiconductors market.

Global Opto-Semiconductors Market Key Region

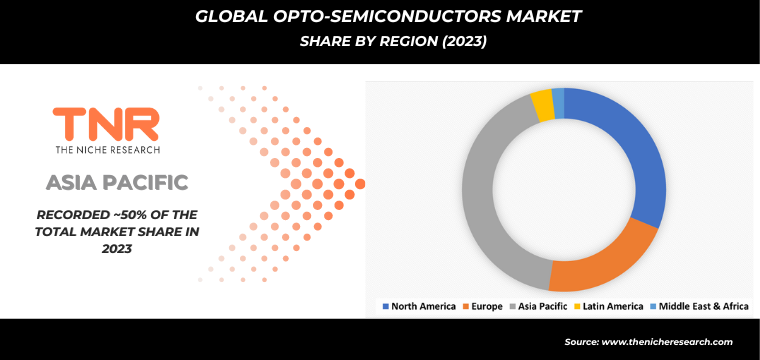

The Asia-Pacific region holds a commanding position in the global opto-semiconductors market, accounting for a substantial ~50% of the market share in 2024. This dominance is largely attributed to several key factors that have positioned the region as the epicenter of growth and innovation in the opto-semiconductors industry.

One of the primary drivers of this opto-semiconductors market dominance is the presence of leading semiconductor manufacturers in the region. Countries like China, Japan, and South Korea are home to some of the world’s largest and most advanced semiconductor companies. For instance, Samsung Electronics and LG Electronics in South Korea, Sony Corporation in Japan, and a range of key players in China, such as BOE Technology and San’an Optoelectronics, are major contributors to the production of opto-semiconductor components like LEDs, laser diodes, and optical sensors. In 2023, the volume of opto-semiconductors produced in the Asia-Pacific region was approximately 40 billion units, a figure that underscores the region’s significant role in the global market. This volume is expected to grow to 65 billion units by 2030, driven by continued advancements in technology and increased demand.

One of the primary drivers of this opto-semiconductors market dominance is the presence of leading semiconductor manufacturers in the region. Countries like China, Japan, and South Korea are home to some of the world’s largest and most advanced semiconductor companies. For instance, Samsung Electronics and LG Electronics in South Korea, Sony Corporation in Japan, and a range of key players in China, such as BOE Technology and San’an Optoelectronics, are major contributors to the production of opto-semiconductor components like LEDs, laser diodes, and optical sensors. In 2023, the volume of opto-semiconductors produced in the Asia-Pacific region was approximately 40 billion units, a figure that underscores the region’s significant role in the global market. This volume is expected to grow to 65 billion units by 2030, driven by continued advancements in technology and increased demand.

Another critical factor is the high demand for consumer electronics in the Asia-Pacific region, particularly in China, which is the world’s largest consumer electronics market. The rapid urbanization and rising disposable incomes in the region have led to a surge in the adoption of smartphones, tablets, televisions, and other electronic devices, all of which rely heavily on opto-semiconductor components. In 2023, China’s consumer electronics market alone was valued at approximately USD 300 billion, with a significant portion of this value attributed to products that incorporate opto-semiconductors.

Government initiatives and policies in the Asia-Pacific region have significantly contributed to market growth. China’s “Made in China 2025” initiative and Japan’s Top Runner Program have supported the semiconductor sector with large-scale investments in manufacturing, R&D, and energy-efficient technologies. In 2023, the volume of opto-semiconductors driven by such initiatives was estimated at 15 billion units. This figure is expected to increase to 25 billion units by 2030, reflecting the positive impact of these supportive policies.

Given these factors, the Asia-Pacific region is expected to continue its dominance in the opto-semiconductors market with a projected compound annual growth rate (CAGR) of 12.7% during the forecast period. This growth rate is driven by ongoing technological advancements, expanding consumer electronics markets, and favorable government policies. As a result, the Asia-Pacific region is likely to remain the leading hub for opto-semiconductor production and innovation, shaping the future of the global market with a projected market volume of approximately ~65 billion units by 2030.

Key companies operating in the global opto-semiconductors market are:

- Broadcom Inc

- Coherent, Inc.

- Hamamatsu Photonics K.K.

- ICTK Holdings

- IPG Photonics

- JENOPTIK

- LITE-ON Technology Corporation

- Littelfuse, Inc.

- Mitsubishi Electric Corporation

- OSRAM

- Renesas electronics corporation

- ROHM Semiconductor

- TOSHIBA Corporation

- TT Electronics plc

- Ushio America, Inc.

- Vishay Intertechnology, Inc.

- Other Industry Participants

Global Opto-Semiconductors Market Key Insights

| Report Specifications | Details |

| Market Revenue in 2023 | US$ 16.86 Bn |

| Market Size Forecast by 2034 | US$ 47.8 Bn |

| Growth Rate (CAGR) | 10.5% |

| Historic Data | 2016 – 2022 |

| Base Year for Estimation | 2023 |

| Forecast Period | 2024 – 2034 |

| Report Inclusions | Market Size & Estimates, Market Dynamics, Competitive Scenario, Trends, Growth Factors, Market Determinants, Key Investment Segmentation, Product/Service/Solutions Benchmarking |

| Segments Covered | By Type, By End Use Industry |

| Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | U.S., Canada, Mexico, Rest of North America, France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe, China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific, Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa, Brazil, Argentina, Rest of Latin America |

| Key Players | Broadcom Inc, Coherent, Inc., Hamamatsu Photonics K.K., ICTK Holdings, IPG Photonics, JENOPTIK, LITE-ON Technology Corporation, Littelfuse, Inc., Mitsubishi Electric Corporation, OSRAM, Renesas electronics corporation, ROHM Semiconductor, TOSHIBA Corporation, TT Electronics plc, Ushio America, Inc., Vishay Intertechnology, Inc., Other Industry Participants |

| Customization Scope | Customization allows for the inclusion/modification of content pertaining to geographical regions, countries, and specific market segments. |

| Pricing & Procurement Options | Explore purchase options tailored to your specific research requirements |

| Contact Details | Consult With Our Expert

Japan (Toll-Free): +81 663-386-8111 South Korea (Toll-Free): +82-808- 703-126 Saudi Arabia (Toll-Free): +966 800-850-1643 United Kingdom: +44 753-710-5080 United States: +1 302-232-5106 E-mail: askanexpert@thenicheresearch.com |

Global Opto-Semiconductors Market Scope

By Type

- Light-Emitting Diodes (LEDs)

- Photodetectors

- Laser Diodes

- Image Sensors

- Solar Cells

- Others

By End Use Industry

- Consumer Electronics

- Automotive Industry

- Industrial Automation in Manufacturing

- Healthcare and Biotechnology

- Energy

- Aerospace and Defence

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

Global Opto-Semiconductors Market Layout

Table of Contents

Note: This ToC is tentative and can be changed according to the research study conducted during the course of report completion.

**Exclusive for Multi-User and Enterprise User.

Global Opto-Semiconductors Market

By Type

- Light-Emitting Diodes (LEDs)

- Photodetectors

- Laser Diodes

- Image Sensors

- Solar Cells

- Others

By End Use Industry

- Consumer Electronics

- Automotive Industry

- Industrial Automation in Manufacturing

- Healthcare and Biotechnology

- Energy

- Aerospace and Defence

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

The Niche Research approach encompasses both primary and secondary research methods to provide comprehensive insights. While primary research is the cornerstone of our studies, we also incorporate secondary research sources such as company annual reports, premium industry databases, press releases, industry journals, and white papers.

Within our primary research, we actively engage with various industry stakeholders, conducting paid interviews and surveys. Our meticulous analysis extends to every market participant in major countries, allowing us to thoroughly examine their portfolios, calculate market shares, and segment revenues.

Our data collection primarily focuses on individual countries within our research scope, enabling us to estimate regional market sizes. Typically, we employ a bottom-up approach, meticulously tracking trends in different countries. We analyze growth drivers, constraints, technological innovations, and opportunities for each country, ultimately arriving at regional figures.Our process begins by examining the growth prospects of each country. Building upon these insights, we project growth and trends for the entire region. Finally, we utilize our proprietary model to refine estimations and forecasts.

Our data validation standards are integral to ensuring the reliability and accuracy of our research findings. Here’s a breakdown of our data validation processes and the stakeholders we engage with during our primary research:

- Supply Side Analysis: We initiate a supply side analysis by directly contacting market participants, through telephonic interviews and questionnaires containing both open-ended and close-ended questions. We gather information on their portfolios, segment revenues, developments, and growth strategies.

- Demand Side Analysis: To gain insights into adoption trends and consumer preferences, we reach out to target customers and users (non-vendors). This information forms a vital part of the qualitative analysis section of our reports, covering market dynamics, adoption trends, consumer behavior, spending patterns, and other related aspects.

- Consultant Insights: We tap into the expertise of our partner consultants from around the world to obtain their unique viewpoints and perspectives. Their insights contribute to a well-rounded understanding of the markets under investigation.

- In-House Validation: To ensure data accuracy and reliability, we conduct cross-validation of data points and information through our in-house team of consultants and utilize advanced data modeling tools for thorough verification.

The forecasts we provide are based on a comprehensive assessment of various factors, including:

- Market Trends and Past Performance (Last Five Years): We accurately analyze market trends and performance data from preceding five years to identify historical patterns and understand the market’s evolution.

- Historical Performance and Growth of Market Participants: We assess the historical performance and growth trajectories of key market participants. This analysis provides insights into the competitive landscape and individual company strategies.

- Market Determinants Impact Analysis (Next Eight Years): We conduct a rigorous analysis of the factors that are projected to influence the market over the next eight years. This includes assessing both internal and external determinants that can shape market dynamics.

- Drivers and Challenges for the Forecast Period:Identify the factors expected to drive market growth during the forecast period, as well as the challenges that the industry may face. This analysis aids in deriving an accurate growth rate projection.

- New Acquisitions, Collaborations, or Partnerships: We keep a close watch on any new acquisitions, collaborations, or partnerships within the industry. These developments can have a significant impact on market dynamics and competitiveness.

- Macro and Micro Factors Analysis:A thorough examination of both macro-level factors (e.g., economic trends, regulatory changes) and micro-level factors (e.g., technological advancements, consumer preferences) that may influence the market during the forecast period.

- End-User Sentiment Analysis: To understand the market from the end-user perspective, we conduct sentiment analysis. This involves assessing the sentiment, preferences, and feedback of the end-users, which can provide valuable insights into market trends.

- Perspective of Primary Participants: Insights gathered directly from primary research participants play a crucial role in shaping our forecasts. Their perspectives and experiences provide valuable qualitative data.

- Year-on-Year Growth Trend: We utilize a year-on-year growth trend based on historical market growth and expected future trends. This helps in formulating our growth projections, aligning them with the market’s historical performance.

Research process adopted by TNR involves multiple stages, including data collection, validation, quality checks, and presentation. It’s crucial that the data and information we provide add value to your existing market understanding and expertise. We have also established partnerships with business consulting, research, and survey organizations across regions and globally to collaborate on regional analysis and data validation, ensuring the highest level of accuracy and reliability in our reports.