Global OTC Consumer Healthcare Market, By Product Type, By Form, By End User, By Distribution Channel, By Region & Segmental Insights Trends and Forecast, By Value (US$ Bn), Volume (Units) 2024 – 2034

- Industry: Healthcare

- Report ID: TNR-110-1310

- Number of Pages: 420

- Table/Charts : Yes

- September, 2024

- Base Year : 2024

- No. of Companies : 10+

- No. of Countries : 29

- Views : 10061

- Covid Impact Covered: Yes

- War Impact Covered: Yes

- Formats : PDF, Excel, PPT

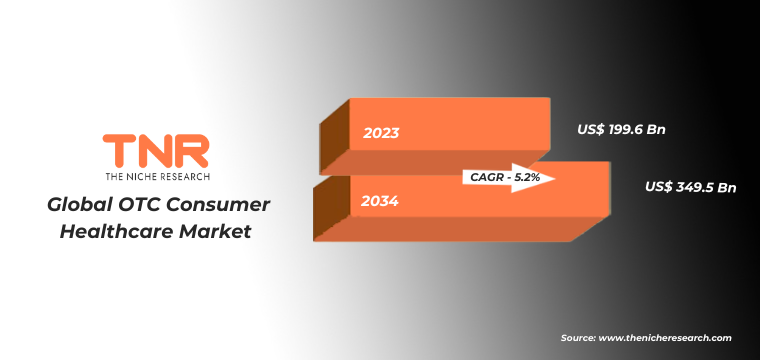

The global OTC (Over-the-Counter) consumer healthcare market encompasses non-prescription medicines, supplements, and personal care products that consumers can buy for self-care. In Terms of Revenue, the Global OTC Consumer Healthcare Market was Worth US$ 199.6 Bn in 2023, Anticipated to Witness CAGR of 5.2% During 2024 – 2034. This market plays a crucial role in day-to-day life by offering accessible healthcare solutions without the need for a doctor’s prescription.

People commonly use OTC products for managing minor ailments such as headaches (e.g., acetaminophen), colds (e.g., cough syrups), and digestive issues (e.g., antacids). The market’s importance extends to different applications, from pain management to immune support through vitamins and supplements. For example, during the COVID-19 pandemic in 2020, demand for immunity-boosting supplements surged globally, emphasizing OTC healthcare’s role in preventive health. This sector supports self-care, reducing pressure on healthcare systems.

OTC Medicines Retail Sales:

In the global OTC consumer healthcare market, retail sales of OTC medicines have shown robust growth, reflecting the increasing consumer preference for self-care solutions. In 2023, the global OTC medicines market saw substantial sales driven by heightened health awareness and convenience.

For instance, the demand for OTC pain relievers and allergy medications surged in the United States, as consumers sought immediate relief without prescription requirements. The widespread availability of OTC products in pharmacies, supermarkets, and online platforms further supports this growth. Additionally, promotional activities and educational campaigns by manufacturers contribute to the rising trend in OTC medicines retail sales.

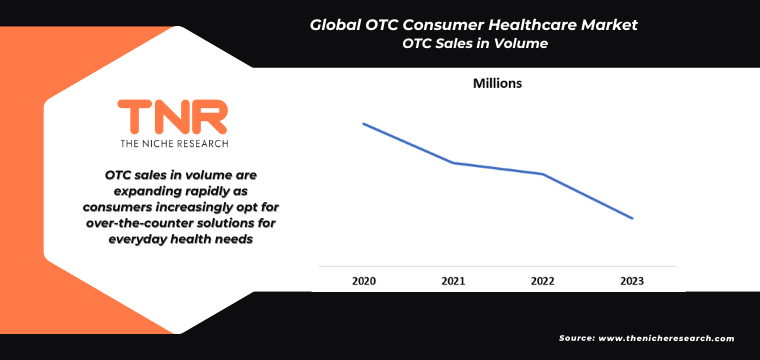

OTC Sales in Volume:

In the global OTC consumer healthcare market, sales volume of OTC products has seen significant growth due to increased consumer adoption of self-medication. In 2023, the volume of OTC sales reached new heights, driven by heightened health awareness and convenience. For example, in Europe, the volume of sales for cold and flu medications surged during the peak winter season, reflecting consumers’ preference for over-the-counter remedies.

Additionally, the expansion of online retail channels has further boosted volume sales by making these products more accessible. The consistent growth in OTC sales volume highlights a shift towards proactive health management among consumers worldwide.

Growth Drivers in the Global OTC Consumer Healthcare Market

- Rising Self-Care Trends: Consumers are increasingly prioritizing self-care, driving demand for over-the-counter (OTC) healthcare products. For example, during the COVID-19 pandemic, in 2020, there was a notable surge in sales of immunity-boosting OTC products like vitamins and supplements.

- Aging Population: The aging global population is fueling growth in the OTC healthcare market, as older adults seek accessible, non-prescription treatments for chronic conditions. In 2021, Europe’s aging demographic led to increased demand for pain relief and digestive health OTC products.

Restraints in the Global OTC Consumer Healthcare Market

- Stringent Regulatory Frameworks: Strict regulations around OTC product approvals can hinder market growth. For example, in 2021, increased regulatory scrutiny by the U.S. FDA slowed the release of new OTC drugs, creating barriers for manufacturers in launching innovative healthcare solutions.

- Consumer Safety Concerns: Rising concerns over potential side effects or misuse of OTC products can limit market expansion. In 2022, growing awareness of drug interactions and side effects associated with OTC pain relievers led to a decline in consumer trust, impacting sales in Europe.

Global OTC Consumer Healthcare Market Segmental Analysis

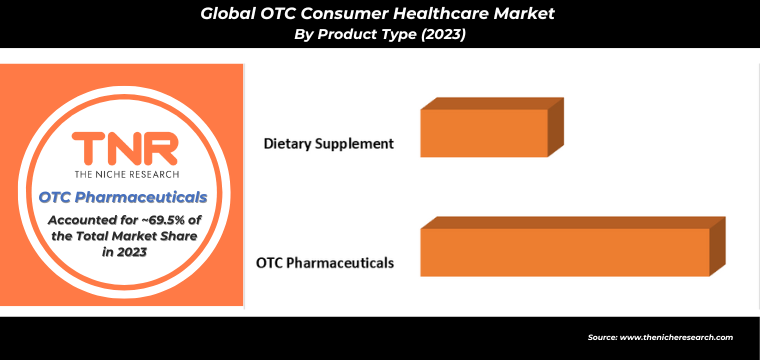

By Product Type: OTC pharmaceuticals have emerged as the dominant product type in the global OTC consumer healthcare market, accounting for 69.5% of revenue share. This growth is largely driven by the increasing consumer preference for self-medication, easy availability, and affordability of these products. For instance, in 2023, the demand for OTC pain relievers and cold medications surged, particularly during flu seasons in the United States, reflecting a shift towards managing minor health issues without prescription drugs. This shift is further supported by the expansion of e-commerce platforms, making OTC medications more accessible to consumers worldwide, thereby strengthening their dominance in the market.

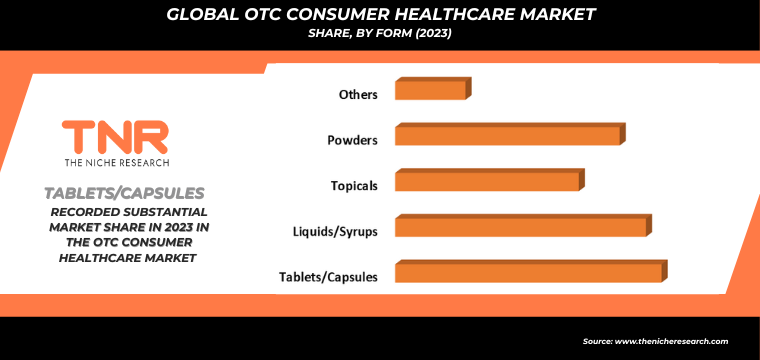

By Form: In 2023, the liquid/syrup segment secured its position as the second-largest form category in the global OTC consumer healthcare market, with a revenue share of 25.2%. This growth is attributed to the segment’s suitability for various age groups, especially children and the elderly, who may have difficulty swallowing pills. For example, liquid cough syrups, widely used during flu seasons, saw increased demand due to their ease of consumption and fast action. Additionally, in regions like Europe, liquid vitamin supplements gained popularity for their enhanced absorption rates, further boosting the segment’s market share and securing its prominent position globally.

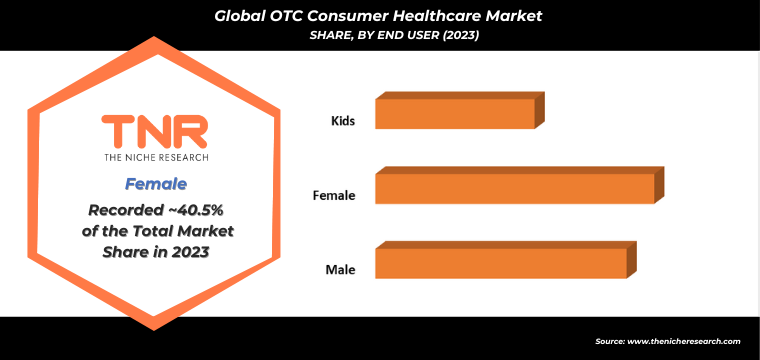

By End User: Male segment is projected to be the fastest-growing end-user category in the global OTC consumer healthcare market, expected to hold a substantial 36.5% revenue share. This growth is driven by increasing health awareness and self-care practices among men. For instance, in 2023, the demand for OTC supplements aimed at male health, such as energy boosters and multivitamins, saw a significant rise in the U.S. market. Additionally, male-focused products like hair growth treatments and sports supplements are becoming more prevalent, contributing to the segment’s substantial revenue growth in the global OTC healthcare market.

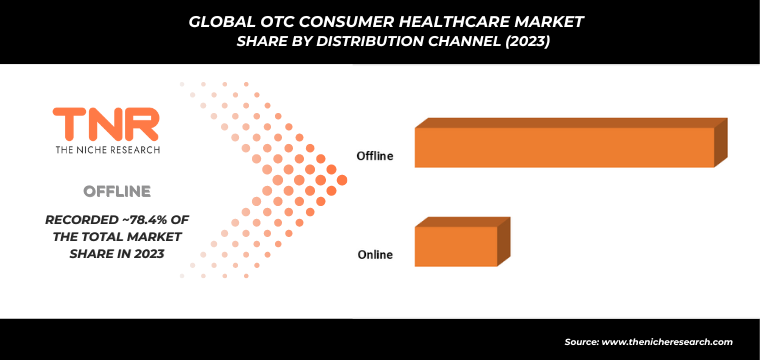

By Distribution Channel: Offline segment dominated the global OTC consumer healthcare market, with a revenue share of 78.4%. This dominance is driven by consumers’ preference for purchasing healthcare products in physical stores, where they can receive immediate assistance and verify product authenticity. In 2023, pharmacies and drugstores continued to be the primary sales channels, especially in regions like Asia-Pacific, where consumers trust in-person consultations with pharmacists. For example, OTC cold and flu medications were heavily purchased offline during seasonal outbreaks, reinforcing the importance of brick-and-mortar stores in the distribution of OTC products globally.

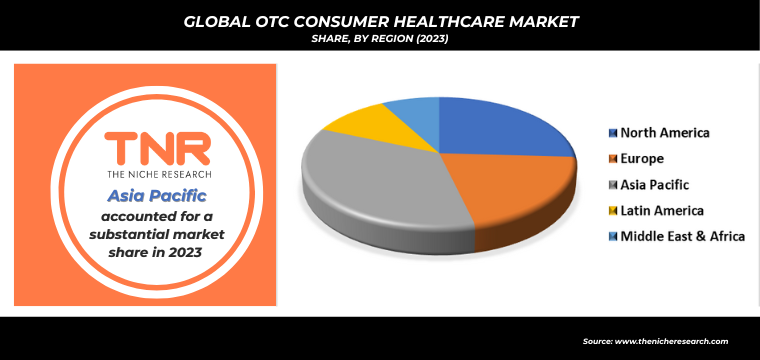

By Region: In 2023, Asia Pacific reinforced its leading position in the global OTC consumer healthcare market, capturing a significant revenue share of 35.2%. This growth is fueled by increasing healthcare awareness, rising disposable incomes, and expanding urban populations in countries like China and India. The region saw heightened demand for OTC vitamins, pain relievers, and digestive aids, particularly in response to health-conscious consumers seeking preventive care. For instance, in China, OTC herbal supplements gained popularity due to their perceived health benefits. Additionally, the expansion of pharmacies and retail chains across Asia Pacific further supported the region’s market dominance.

Competitive Landscape

Some of the players operating in the OTC Consumer Healthcare Market are

- Abbott Laboratories

- Bayer AG

- GlaxoSmithKline (GSK) Consumer Healthcare

- Haleon (formerly GSK Consumer Healthcare)

- Johnson & Johnson

- Nestlé Health Science

- Perrigo Company plc

- Pfizer Inc.

- Procter & Gamble (P&G)

- Reckitt Benckiser Group

- Sanofi S.A.

- Sun Pharmaceutical Industries Ltd.

- Taisho Pharmaceutical

- Takeda Pharmaceutical Company

- Unilever

- Other Industry Participants

Global OTC Consumer Healthcare Market Scope:

| Report Specifications | Details |

| Market Revenue in 2023 | US$ 199.6 Bn |

| Market Size Forecast by 2034 | US$ 348.5 Bn |

| Growth Rate (CAGR) | 5.2% |

| Historic Data | 2016 – 2022 |

| Base Year for Estimation | 2023 |

| Forecast Period | 2024 – 2034 |

| Report Inclusions | Market Size & Estimates, Market Dynamics, Competitive Scenario, Trends, Growth Factors, Market Determinants, Key Investment Segmentation, Product/Service/Solutions Benchmarking |

| Segments Covered | By Product Type, By Form, By End User, By Distribution Channel, By Region |

| Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | U.S., Canada, Mexico, Rest of North America, France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe, China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific, Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa, Brazil, Argentina, Rest of Latin America |

| Key Players | Abbott Laboratories, Bayer AG, GlaxoSmithKline (GSK), Johnson & Johnson, Nestlé Health Science, Perrigo Company plc, Pfizer Inc., Procter & Gamble (P&G), Reckitt Benckiser Group, Sanofi S.A., Sun Pharmaceutical Industries Ltd., Taisho Pharmaceutical, Takeda Pharmaceutical Company, Unilever |

| Customization Scope | Customization allows for the inclusion/modification of content pertaining to geographical regions, countries, and specific market segments. |

| Pricing & Procurement Options | Explore purchase options tailored to your specific research requirements |

| Contact Details | Consult With Our Expert

Japan (Toll-Free): +81 663-386-8111 South Korea (Toll-Free): +82-808- 703-126 Saudi Arabia (Toll-Free): +966 800-850-1643 United Kingdom: +44 753-710-5080 United States: +1 302-232-5106 E-mail: askanexpert@thenicheresearch.com

|

Global OTC Consumer Healthcare Market

By Product Type

- OTC Pharmaceuticals

- Eye Care

- Wound Care

- Oral Healthcare

- Medicated Skin Care

- Digestive Remedies

- Wound Care

- Intimate Care

- Hair Care

- Skin Care

- Analgesic

- Cough, Cold and Allergy Remedies

- Others

- Dietary Supplement

- Vitamin

- Protien

- Minerals

- Nutrition

- Others

By Form

- Tablets/Capsules

- Liquids/Syrups

- Topicals

- Powders

- Others

By End User

- Male

- Female

- Kids

By Distribution Channel

- Online

- Offline

- Pharmacies and Drugstores

- Specialty Stores

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

Report Layout:

Table of Contents

**Exclusive for Multi-User and Enterprise User.

Global OTC Consumer Healthcare Market

By Product Type

- OTC Pharmaceuticals

- Eye Care

- Wound Care

- Oral Healthcare

- Medicated Skin Care

- Digestive Remedies

- Wound Care

- Intimate Care

- Hair Care

- Skin Care

- Analgesic

- Cough, Cold and Allergy Remedies

- Others

- Dietary Supplement

- Vitamin

- Protien

- Minerals

- Nutrition

- Others

By Form

- Tablets/Capsules

- Liquids/Syrups

- Topicals

- Powders

- Others

By End User

- Male

- Female

- Kids

By Distribution Channel

- Online

- Offline

- Pharmacies and Drugstores

- Specialty Stores

- Others

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

The Niche Research approach encompasses both primary and secondary research methods to provide comprehensive insights. While primary research is the cornerstone of our studies, we also incorporate secondary research sources such as company annual reports, premium industry databases, press releases, industry journals, and white papers.

Within our primary research, we actively engage with various industry stakeholders, conducting paid interviews and surveys. Our meticulous analysis extends to every market participant in major countries, allowing us to thoroughly examine their portfolios, calculate market shares, and segment revenues.

Our data collection primarily focuses on individual countries within our research scope, enabling us to estimate regional market sizes. Typically, we employ a bottom-up approach, meticulously tracking trends in different countries. We analyze growth drivers, constraints, technological innovations, and opportunities for each country, ultimately arriving at regional figures.Our process begins by examining the growth prospects of each country. Building upon these insights, we project growth and trends for the entire region. Finally, we utilize our proprietary model to refine estimations and forecasts.

Our data validation standards are integral to ensuring the reliability and accuracy of our research findings. Here’s a breakdown of our data validation processes and the stakeholders we engage with during our primary research:

- Supply Side Analysis: We initiate a supply side analysis by directly contacting market participants, through telephonic interviews and questionnaires containing both open-ended and close-ended questions. We gather information on their portfolios, segment revenues, developments, and growth strategies.

- Demand Side Analysis: To gain insights into adoption trends and consumer preferences, we reach out to target customers and users (non-vendors). This information forms a vital part of the qualitative analysis section of our reports, covering market dynamics, adoption trends, consumer behavior, spending patterns, and other related aspects.

- Consultant Insights: We tap into the expertise of our partner consultants from around the world to obtain their unique viewpoints and perspectives. Their insights contribute to a well-rounded understanding of the markets under investigation.

- In-House Validation: To ensure data accuracy and reliability, we conduct cross-validation of data points and information through our in-house team of consultants and utilize advanced data modeling tools for thorough verification.

The forecasts we provide are based on a comprehensive assessment of various factors, including:

- Market Trends and Past Performance (Last Five Years): We accurately analyze market trends and performance data from preceding five years to identify historical patterns and understand the market’s evolution.

- Historical Performance and Growth of Market Participants: We assess the historical performance and growth trajectories of key market participants. This analysis provides insights into the competitive landscape and individual company strategies.

- Market Determinants Impact Analysis (Next Eight Years): We conduct a rigorous analysis of the factors that are projected to influence the market over the next eight years. This includes assessing both internal and external determinants that can shape market dynamics.

- Drivers and Challenges for the Forecast Period:Identify the factors expected to drive market growth during the forecast period, as well as the challenges that the industry may face. This analysis aids in deriving an accurate growth rate projection.

- New Acquisitions, Collaborations, or Partnerships: We keep a close watch on any new acquisitions, collaborations, or partnerships within the industry. These developments can have a significant impact on market dynamics and competitiveness.

- Macro and Micro Factors Analysis:A thorough examination of both macro-level factors (e.g., economic trends, regulatory changes) and micro-level factors (e.g., technological advancements, consumer preferences) that may influence the market during the forecast period.

- End-User Sentiment Analysis: To understand the market from the end-user perspective, we conduct sentiment analysis. This involves assessing the sentiment, preferences, and feedback of the end-users, which can provide valuable insights into market trends.

- Perspective of Primary Participants: Insights gathered directly from primary research participants play a crucial role in shaping our forecasts. Their perspectives and experiences provide valuable qualitative data.

- Year-on-Year Growth Trend: We utilize a year-on-year growth trend based on historical market growth and expected future trends. This helps in formulating our growth projections, aligning them with the market’s historical performance.

Research process adopted by TNR involves multiple stages, including data collection, validation, quality checks, and presentation. It’s crucial that the data and information we provide add value to your existing market understanding and expertise. We have also established partnerships with business consulting, research, and survey organizations across regions and globally to collaborate on regional analysis and data validation, ensuring the highest level of accuracy and reliability in our reports.