Global Preclinical Imaging Market: By Product Type, By Application, By End User By Region & Segmental Insights Trends and Forecast, 2024 – 2034

- Industry: Healthcare

- Report ID: TNR-110-1150

- Number of Pages: 420

- Table/Charts : Yes

- June, 2024

- Base Year : 2024

- No. of Companies : 10+

- No. of Countries : 29

- Views : 10043

- Covid Impact Covered: Yes

- War Impact Covered: Yes

- Formats : PDF, Excel, PPT

Preclinical imaging involves the use of advanced imaging technologies to study biological processes in animal models before clinical trials in humans. This field employs techniques such as MRI, PET, CT, and optical imaging to visualize and monitor the anatomy, physiology, and molecular activities within these models. Preclinical imaging provides crucial insights into disease mechanisms, drug efficacy, and safety, allowing researchers to gather detailed, real-time data on how new treatments interact with living systems. By enabling non-invasive, precise observation of biological changes, preclinical imaging plays a vital role in the early stages of drug development, helping to identify promising therapeutic candidates and streamline the path to clinical application.

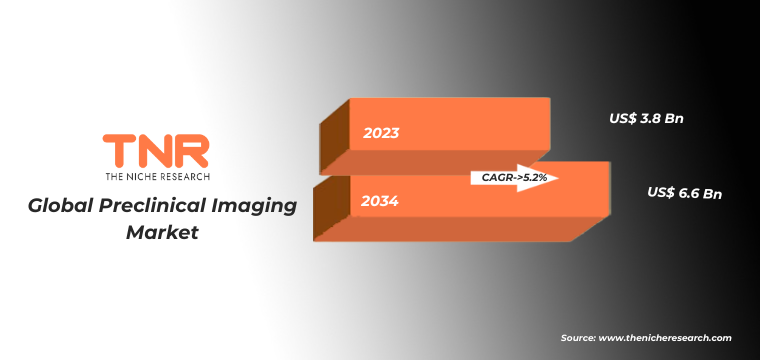

The demand for preclinical imaging is driven by the need for precise, non-invasive visualization of biological processes in animal models, essential for advancing drug development and medical research. Technological advancements in imaging modalities such as MRI, PET, and CT have significantly improved the accuracy and detail of preclinical studies. The rising prevalence of chronic diseases and the growing focus on personalized medicine further fuel this demand, as detailed imaging is crucial for understanding disease mechanisms and evaluating therapeutic efficacy. Additionally, stringent regulatory requirements for drug approval necessitate comprehensive preclinical imaging to ensure safety and effectiveness, making it a critical component of the pharmaceutical and biotechnology research pipeline. In terms of revenue, the global preclinical imaging market was worth US$ 3.8 Bn in 2023, anticipated to witness CAGR of 5.2% during 2024 – 2034.

Global Preclinical Imaging Market Dynamics

Technological Advancements: Innovations in imaging technologies, such as high-resolution MRI, PET, CT, and optical imaging, enhance the accuracy and efficiency of preclinical studies. These advancements enable more detailed visualization of biological processes, driving demand for state-of-the-art imaging systems. Growth in emerging economies, with increased focus on healthcare infrastructure and research capabilities, presents new opportunities for market expansion.

Rising Prevalence of Chronic Diseases: The increasing incidence of chronic diseases, such as cancer, cardiovascular diseases, and neurodegenerative disorders, necessitates extensive preclinical research to develop effective treatments, thus boosting the demand for preclinical imaging. The global increase in the elderly population contributes to the prevalence of age-related diseases, leading to heightened demand for preclinical imaging in the development of geriatric therapies.

Pharmaceutical and Biotechnology R&D: The robust pipeline of new drug candidates and therapeutic interventions in the pharmaceutical and biotechnology sectors fuels the need for comprehensive preclinical imaging to evaluate the safety and efficacy of these innovations. Strategic collaborations and partnerships among academic institutions, research organizations, and industry players promote the development and adoption of cutting-edge imaging technologies, further driving market dynamics.

Regulatory Requirements: Stringent regulatory guidelines for drug approval mandate thorough preclinical testing, including imaging studies, to ensure drug safety and effectiveness, thereby driving market growth. Increased investment in biomedical research by governments and private entities supports the expansion of preclinical imaging capabilities, fostering market growth.

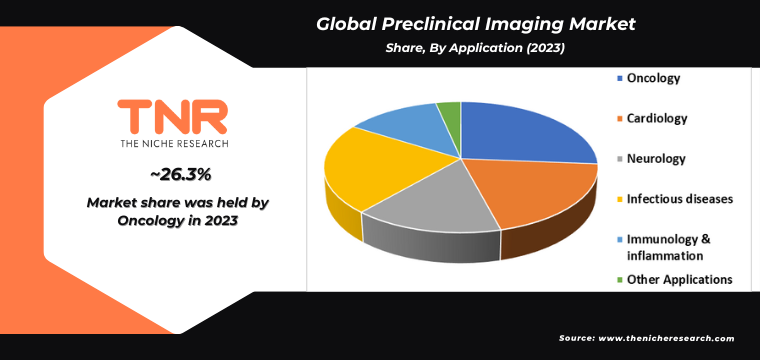

Oncology Segment has Garnered Major Market Share in the Global Preclinical Imaging Market During the Forecast Period (2024 – 2034).

Oncology research is a significant driver of the demand for preclinical imaging, fueled by the urgent need to develop more effective cancer treatments. Preclinical imaging technologies such as MRI, PET, and CT scans are pivotal in visualizing and tracking tumor development, metastasis, and response to therapies in animal models. These advanced imaging methods provide detailed, real-time insights into the biological behavior of cancers, enabling researchers to better understand tumor biology and the efficacy of new oncologic drugs. The rising incidence of cancer worldwide intensifies the pressure to discover novel therapies, thus amplifying the need for thorough preclinical evaluations. Moreover, the push for personalized medicine in oncology necessitates precise imaging to identify specific biomarkers and tailor treatments accordingly. As the complexity of cancer treatments increases, so does the reliance on sophisticated preclinical imaging to guide drug development, optimize therapeutic strategies, and ultimately improve patient outcomes.

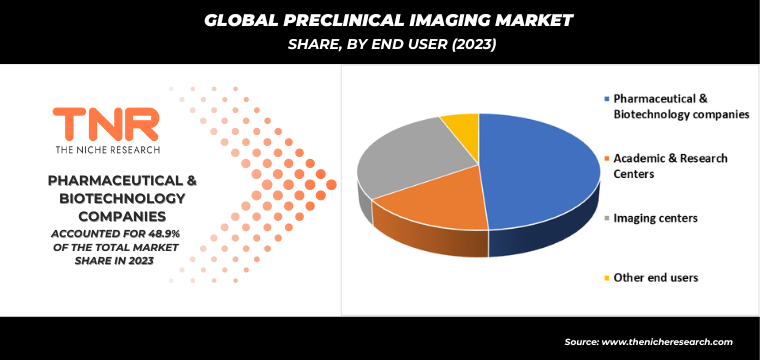

By End User Pharmaceutical and Biotechnology Companies Segment had the Highest Share in the Global Preclinical Imaging Market in 2023.

Pharmaceutical and biotechnology companies are key drivers of the demand for preclinical imaging due to their relentless pursuit of innovative drug development and therapeutic solutions. These companies rely on advanced imaging technologies, such as MRI, PET, and CT scans, to obtain detailed insights into the efficacy and safety of new compounds in animal models before proceeding to human trials. The precise data garnered from these imaging modalities are crucial for understanding disease mechanisms, optimizing drug candidates, and predicting clinical outcomes. Moreover, the rising prevalence of chronic and complex diseases necessitates more comprehensive preclinical studies, further escalating the need for sophisticated imaging techniques. Additionally, stringent regulatory standards require thorough preclinical validation to minimize risks and enhance the likelihood of successful clinical trials. As these companies strive to expedite drug discovery and development processes, the demand for cutting-edge preclinical imaging continues to grow, ensuring high-quality, cost-effective research outcomes.

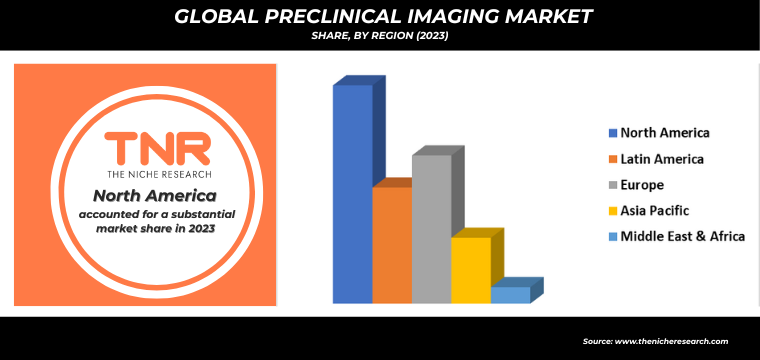

By Region, North America Dominated the Global Preclinical Imaging Market in 2023.

The demand for preclinical imaging in North America is driven by several key factors, primarily advancements in medical research and drug development. This region’s robust pharmaceutical and biotechnology sectors rely heavily on preclinical imaging to visualize, monitor, and understand biological processes in animal models before human trials. Innovations in imaging technologies, such as MRI, PET, and CT scans, have enhanced the precision and reliability of data, leading to more effective and targeted therapeutic interventions. Additionally, the increasing prevalence of chronic diseases and the aging population have spurred the need for novel treatments, further boosting the demand for comprehensive preclinical studies. Regulatory requirements for drug approval and the emphasis on reducing clinical trial failures also contribute significantly to this demand, as thorough preclinical imaging can help identify potential issues early in the development pipeline, ultimately saving time and resources.

Competitive Landscape: Global Preclinical Imaging Market:

- Agilent Technologies

- Bruker Corporation

- General Electric (GE)

- Mediso Ltd.

- MILabs B.V.

- Molecubes

- MR Solutions

- PerkinElmer, Inc.

- Siemens A.G.

- TriFoil Imaging

- VisualSonics Inc. (Fujifilm)

- Other Industry Participants

Global Preclinical Imaging Market Scope

| Report Specifications | Details |

| Market Revenue in 2023 | US$ 3.8 Bn |

| Market Size Forecast by 2034 | US$ 6.6 Bn |

| Growth Rate (CAGR) | 5.2% |

| Historic Data | 2016 – 2022 |

| Base Year for Estimation | 2023 |

| Forecast Period | 2024 – 2034 |

| Report Inclusions | Market Size & Estimates, Market Dynamics, Competitive Scenario, Trends, Growth Factors, Market Determinants, Key Investment Segmentation, Product/Service/Solutions Benchmarking |

| Segments Covered | By Product Type, By Application, By End User By Region |

| Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | U.S., Canada, Mexico, Rest of North America, France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe, China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific, Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa, Brazil, Argentina, Rest of Latin America |

| Key Players | Agilent Technologies, Bruker Corporation, General Electric (GE), Mediso Ltd., MILabs B.V., Molecubes, MR Solutions, PerkinElmer, Inc., Siemens A.G., TriFoil Imaging, VisualSonics Inc. (Fujifilm) |

| Customization Scope | Customization allows for the inclusion/modification of content pertaining to geographical regions, countries, and specific market segments. |

| Pricing & Procurement Options | Explore purchase options tailored to your specific research requirements |

| Contact Details | Consult With Our Expert

Japan (Toll-Free): +81 663-386-8111 South Korea (Toll-Free): +82-808- 703-126 Saudi Arabia (Toll-Free): +966 800-850-1643 United Kingdom: +44 753-710-5080 United States: +1 302-232-5106 E-mail: askanexpert@thenicheresearch.com

|

Global Preclinical Imaging Market

By Product Type

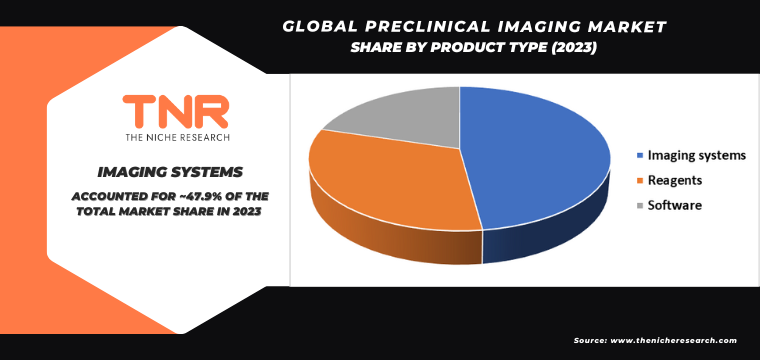

- Imaging systems

- Optical imaging systems

- Bioluminescence imaging systems

- Fluorescence imaging systems

- Other optical imaging systems

- Nuclear imaging systems

- micro-pet imaging systems

- Standalone pet imaging systems

- Pet/CT imaging systems

- Pet/MRI imaging systems

- Micro-spect imaging systems

- standalone spet imaging systems

- spet/ct imaging systems

- spet/ MRI imaging systems

- Trimodality (spect/pet/ct) imaging systems

- micro-pet imaging systems

- Micro-MRI systems

- Micro-ultrasound systems

- Micro-ct systems

- Photoacoustic imaging systems

- Magnetic particle imaging (mpi) systems

- Optical imaging systems

- Reagents

- Preclinical optical imaging reagents

- Preclinical bioluminescent imaging reagents

- Luciferins

- Coelenterazne

- Furimazine

- Preclinical fluorescent imaging reagents

- Green fluorescent proteins

- Red fluorescent proteins

- Infrared dyes

- Preclinical nuclear imaging reagents

- Preclinical pet tracers

- Fluorine-18-based preclinical pet tracers

- Carbon-11-based preclinical pet tracers

- Copper-64-based preclinical pet tracers

- Other pet tracers

- Preclinical spect probes

- Technetium-99m-based preclinical spect probes

- Iodine-131-based preclinical spect probes

- Gallium-67-based preclinical spect probes

- Thallium-201-based preclinical spect probes

- Other spect probes

- Preclinical MRI contrast agents

- Gadolinium-based preclinical contrast agents

- Iron-based preclinical contrast agents

- Manganese-based preclinical contrast agents

- Preclinical ultrasound contrast agents

- Preclinical CT contrast agents

- Iodine-based preclinical ct contrast agents

- Barium-based preclinical ct contrast agents

- Gold nanoparticles

- Gastrografin-based preclinical ct contrast agents

- Software

- Preclinical pet tracers

By Application

- Oncology

- Cardiology

- Neurology

- Infectious diseases

- Immunology & inflammation

- Other Applications

By End User

- Pharmaceutical & biotechnology companies

- Academic & research centers

- Imaging centers

- Other end users

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

Report Layout:

Table of Contents

Note: This ToC is tentative and can be changed according to the research study conducted during the course of report completion.

**Exclusive for Multi-User and Enterprise User.

Global Preclinical Imaging Market

By Product Type

- Imaging systems

- Optical imaging systems

- Bioluminescence imaging systems

- Fluorescence imaging systems

- Other optical imaging systems

- Nuclear imaging systems

- micro-pet imaging systems

- Standalone pet imaging systems

- Pet/CT imaging systems

- Pet/MRI imaging systems

- Micro-spect imaging systems

- standalone spet imaging systems

- spet/ct imaging systems

- spet/ MRI imaging systems

- Trimodality (spect/pet/ct) imaging systems

- micro-pet imaging systems

- Micro-MRI systems

- Micro-ultrasound systems

- Micro-ct systems

- Photoacoustic imaging systems

- Magnetic particle imaging (mpi) systems

- Optical imaging systems

- Reagents

- Preclinical optical imaging reagents

- Preclinical bioluminescent imaging reagents

- Luciferins

- Coelenterazne

- Furimazine

- Preclinical fluorescent imaging reagents

- Green fluorescent proteins

- Red fluorescent proteins

- Infrared dyes

- Preclinical nuclear imaging reagents

- Preclinical pet tracers

- Fluorine-18-based preclinical pet tracers

- Carbon-11-based preclinical pet tracers

- Copper-64-based preclinical pet tracers

- Other pet tracers

- Preclinical spect probes

- Technetium-99m-based preclinical spect probes

- Iodine-131-based preclinical spect probes

- Gallium-67-based preclinical spect probes

- Thallium-201-based preclinical spect probes

- Other spect probes

- Preclinical MRI contrast agents

- Gadolinium-based preclinical contrast agents

- Iron-based preclinical contrast agents

- Manganese-based preclinical contrast agents

- Preclinical ultrasound contrast agents

- Preclinical CT contrast agents

- Iodine-based preclinical ct contrast agents

- Barium-based preclinical ct contrast agents

- Gold nanoparticles

- Gastrografin-based preclinical ct contrast agents

- Software

- Preclinical pet tracers

By Application

- Oncology

- Cardiology

- Neurology

- Infectious diseases

- Immunology & inflammation

- Other Applications

By End User

- Pharmaceutical & biotechnology companies

- Academic & research centers

- Imaging centers

- Other end users

By Region

- North America (U.S., Canada, Mexico, Rest of North America)

- Europe (France, The UK, Spain, Germany, Italy, Nordic Countries (Denmark, Finland, Iceland, Sweden, Norway), Benelux Union (Belgium, The Netherlands, Luxembourg), Rest of Europe)

- Asia Pacific (China, Japan, India, New Zealand, Australia, South Korea, Southeast Asia (Indonesia, Thailand, Malaysia, Singapore, Rest of Southeast Asia), Rest of Asia Pacific)

- Middle East & Africa (Saudi Arabia, UAE, Egypt, Kuwait, South Africa, Rest of Middle East & Africa)

- Latin America (Brazil, Argentina, Rest of Latin America)

The Niche Research approach encompasses both primary and secondary research methods to provide comprehensive insights. While primary research is the cornerstone of our studies, we also incorporate secondary research sources such as company annual reports, premium industry databases, press releases, industry journals, and white papers.

Within our primary research, we actively engage with various industry stakeholders, conducting paid interviews and surveys. Our meticulous analysis extends to every market participant in major countries, allowing us to thoroughly examine their portfolios, calculate market shares, and segment revenues.

Our data collection primarily focuses on individual countries within our research scope, enabling us to estimate regional market sizes. Typically, we employ a bottom-up approach, meticulously tracking trends in different countries. We analyze growth drivers, constraints, technological innovations, and opportunities for each country, ultimately arriving at regional figures.Our process begins by examining the growth prospects of each country. Building upon these insights, we project growth and trends for the entire region. Finally, we utilize our proprietary model to refine estimations and forecasts.

Our data validation standards are integral to ensuring the reliability and accuracy of our research findings. Here’s a breakdown of our data validation processes and the stakeholders we engage with during our primary research:

- Supply Side Analysis: We initiate a supply side analysis by directly contacting market participants, through telephonic interviews and questionnaires containing both open-ended and close-ended questions. We gather information on their portfolios, segment revenues, developments, and growth strategies.

- Demand Side Analysis: To gain insights into adoption trends and consumer preferences, we reach out to target customers and users (non-vendors). This information forms a vital part of the qualitative analysis section of our reports, covering market dynamics, adoption trends, consumer behavior, spending patterns, and other related aspects.

- Consultant Insights: We tap into the expertise of our partner consultants from around the world to obtain their unique viewpoints and perspectives. Their insights contribute to a well-rounded understanding of the markets under investigation.

- In-House Validation: To ensure data accuracy and reliability, we conduct cross-validation of data points and information through our in-house team of consultants and utilize advanced data modeling tools for thorough verification.

The forecasts we provide are based on a comprehensive assessment of various factors, including:

- Market Trends and Past Performance (Last Five Years): We accurately analyze market trends and performance data from preceding five years to identify historical patterns and understand the market’s evolution.

- Historical Performance and Growth of Market Participants: We assess the historical performance and growth trajectories of key market participants. This analysis provides insights into the competitive landscape and individual company strategies.

- Market Determinants Impact Analysis (Next Eight Years): We conduct a rigorous analysis of the factors that are projected to influence the market over the next eight years. This includes assessing both internal and external determinants that can shape market dynamics.

- Drivers and Challenges for the Forecast Period:Identify the factors expected to drive market growth during the forecast period, as well as the challenges that the industry may face. This analysis aids in deriving an accurate growth rate projection.

- New Acquisitions, Collaborations, or Partnerships: We keep a close watch on any new acquisitions, collaborations, or partnerships within the industry. These developments can have a significant impact on market dynamics and competitiveness.

- Macro and Micro Factors Analysis:A thorough examination of both macro-level factors (e.g., economic trends, regulatory changes) and micro-level factors (e.g., technological advancements, consumer preferences) that may influence the market during the forecast period.

- End-User Sentiment Analysis: To understand the market from the end-user perspective, we conduct sentiment analysis. This involves assessing the sentiment, preferences, and feedback of the end-users, which can provide valuable insights into market trends.

- Perspective of Primary Participants: Insights gathered directly from primary research participants play a crucial role in shaping our forecasts. Their perspectives and experiences provide valuable qualitative data.

- Year-on-Year Growth Trend: We utilize a year-on-year growth trend based on historical market growth and expected future trends. This helps in formulating our growth projections, aligning them with the market’s historical performance.

Research process adopted by TNR involves multiple stages, including data collection, validation, quality checks, and presentation. It’s crucial that the data and information we provide add value to your existing market understanding and expertise. We have also established partnerships with business consulting, research, and survey organizations across regions and globally to collaborate on regional analysis and data validation, ensuring the highest level of accuracy and reliability in our reports.